What Is Insurance Verification and Why It Matters

The Qualigenix Editorial Team consists of certified billing and coding experts with over 40 years of experience across 38+ medical specialties. Our content is rigorously researched against CMS, AMA, and payer-specific guidelines to ensure total compliance and accuracy. We apply the same elite standards to our resources as we do our client work, consistently delivering high claim accuracy and significant reductions in AR days.

Insurance verification is the front-end process that determines whether a claim will be paid before the patient ever enters the exam room. It confirms that the patient’s coverage is active, the correct payer is on file, the planned services are covered benefits, prior authorization is required, and the patient’s financial responsibility is accurately estimated. When verification is done correctly before every visit, eligibility-related claim denials become rare. When it’s skipped for established patients, or done manually and inconsistently, coverage changes slip through and generate a category of denials that takes weeks to investigate and resolve at a cost that consistently exceeds what the verification itself would have taken. The billing problem everyone sees in the denial queue often started at the front desk, days or weeks earlier, when verification didn’t happen.

A patient checks in for a follow-up appointment. They’ve been coming to this practice for three years. The front desk assistant recognizes them, confirms their name and date of birth, and sends them back to the waiting area without pulling their insurance card. The insurance on file was confirmed at their last visit six months ago.

What the front desk doesn’t know is that the patient changed employers four months ago. Their new employer’s health plan is with a completely different insurer. The plan they had six months ago terminated when they left their previous job. The claim submits to the prior insurer. It denies for inactive coverage. The practice’s billing team spends three days investigating the denial, identifies the coverage change, contacts the patient for new insurance information, updates the record, and resubmits. The patient’s new plan has a 90-day timely filing window. The investigation took 21 days. The resubmission has 69 days remaining.

That entire sequence is investigation, the patient contact, the record update, the resubmission, the remaining filing window anxiety — was preventable with a 30-second question at check-in: “Has your insurance changed since your last visit?”

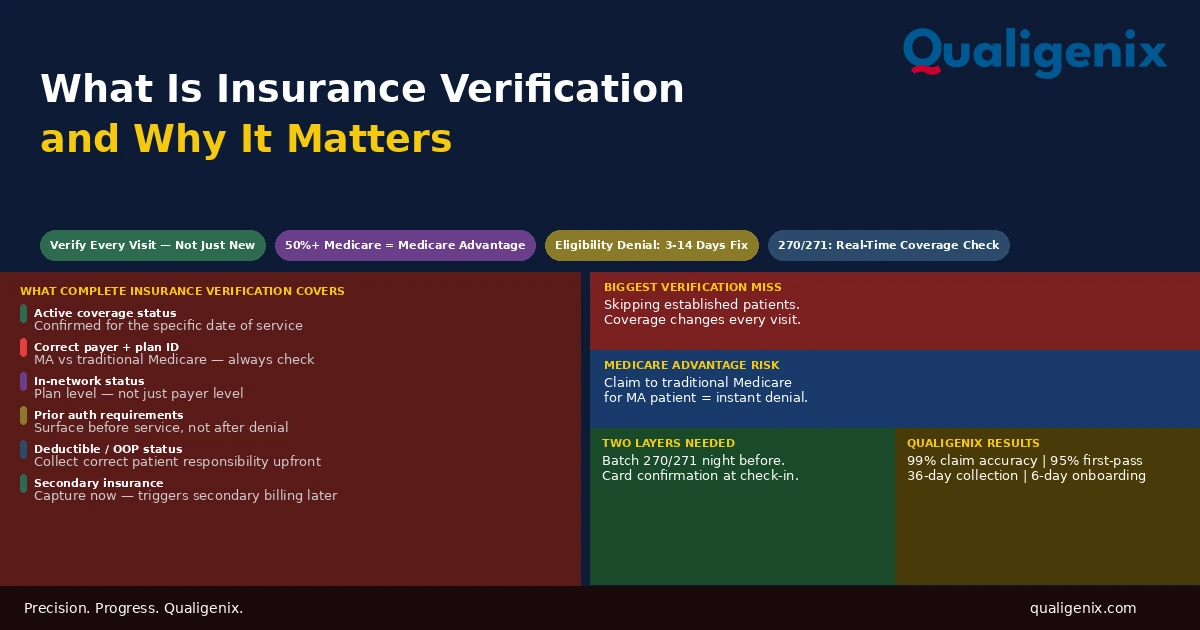

Insurance verification is the process of confirming a patient’s insurance coverage is active and determining the specific benefits applicable to planned services before the encounter. It confirms active coverage status, correct payer and plan, in-network status for the provider, prior authorization requirements, deductible and out-of-pocket status, patient copay and coinsurance, and secondary insurance. Verification must happen before every visit for every patient not just new patients because coverage changes continuously and the cost of an eligibility denial downstream exceeds the cost of verification upstream by a wide margin.

Insurance Verification: Key Facts and Benchmarks

| Metric | Data Point | Source / Context |

|---|---|---|

| Eligibility denials as share of total denials | Approximately 10% to 15% | Medical billing denial analysis |

| Time to resolve one eligibility denial | 3 to 14 days average | Billing operations benchmarks |

| Cost per eligibility denial investigation and resubmission | $25 to $60 per claim | HFMA denial cost analysis |

| Medicare Advantage enrollment (2025) | Over 50% of Medicare beneficiaries | CMS Medicare enrollment data |

| MA enrollees who change plans annually | Approximately 10% to 15% | CMS Medicare Advantage enrollment data |

| 270/271 eligibility transaction response time | Real-time or within seconds | HIPAA EDI transaction standards |

| Recommended pre-visit verification window | 24 to 48 hours before appointment | Revenue cycle best practices |

| Verification frequency recommendation | Every visit — not only new patients | MGMA billing standards |

| Qualigenix claim accuracy rate | 99% | Qualigenix performance data |

| Qualigenix first-pass acceptance rate | 95% | Qualigenix performance data |

| Qualigenix average collection cycle | 36 days | Qualigenix performance data |

| Qualigenix client onboarding time | 6 days | Qualigenix operations data |

What Insurance Verification Actually Covers

Insurance verification is often described as confirming that a patient’s insurance is active. That is the minimum it covers. Complete insurance verification confirms a full set of information that the billing and front-desk workflows depend on to produce a clean claim and collect the correct patient responsibility.

Active Coverage Status

The most basic verification function: is the patient’s insurance plan active on the date of service? A plan that was active yesterday may be inactive today through employer termination, Medicaid redetermination, or COBRA non-payment. A plan that is active today may be terminated by next week. Verification confirms active status for the specific date of service, not just a general sense that the patient has insurance.

Correct Payer and Plan Identification

Verification confirms not just that coverage is active but that the payer and specific plan on file match the patient’s current coverage. This is where the Medicare to Medicare Advantage transition creates the most common payer identification failure. A patient enrolled in traditional Medicare who switches to a Medicare Advantage plan during the annual election period now has private insurance that must be billed to the specific Medicare Advantage plan, not to traditional Medicare. The electronic Medicare eligibility check through the CMS portal distinguishes between traditional Medicare and MA enrollment and identifies the specific MA plan but only if the verification is run.

In-Network Status

Verification confirms whether the rendering provider is in-network under the patient’s specific plan not just the insurer but the specific plan product. A provider can be in-network for a payer’s standard PPO while being out-of-network for the same payer’s narrow network, HMO, or tiered-benefit product. These distinctions matter enormously for the patient’s cost-sharing and for whether the claim will be paid at the contracted rate or treated as an out-of-network service.

In-network status must be verified at the plan level, not the payer level. Being contracted with Blue Shield is not the same as being in-network for every Blue Shield plan product. Many payers offer multiple network tiers broad PPO, narrow network, HMO, EPO, tiered specialty with different provider participation lists for each. A provider who is in-network for the payer but not for the patient’s specific plan product has an out-of-network encounter that generates higher patient cost-sharing and potential claim adjudication disputes that could have been disclosed and addressed before the visit.

Prior Authorization Requirements

Verification identifies whether any services planned for the visit require prior authorization under the patient’s specific plan. This is a critical pre-service step for specialty practices where authorization requirements vary significantly by plan type and service category. When verification surfaces an authorization requirement, the practice can initiate the authorization process before the patient arrives rather than after the service is delivered preventing the authorization-related denial that would otherwise result from a service delivered without an approved authorization.

Deductible and Out-of-Pocket Status

Verification returns the patient’s current deductible balance how much of the deductible has been met for the plan year and how much remains. This information determines whether the patient owes a copay, a percentage coinsurance, or the full charge up to the deductible depending on the plan structure. Collecting the correct patient responsibility at time of service rather than billing the patient afterward improves collection rates on patient balances and reduces the administrative cost of billing patients who didn’t expect a balance.

Referral Requirements

Some plans particularly HMOs require a referral from the patient’s primary care physician before a specialist visit is covered. Verification identifies whether the patient’s plan requires a referral for the planned service. If a referral is required and not obtained, the specialist visit may be denied or the patient may be responsible for the full cost as an out-of-plan service. Identifying this requirement before the encounter allows the practice to confirm the referral is in place or direct the patient to obtain one before the appointment is confirmed.

Secondary Insurance

Verification should identify whether the patient has secondary insurance coverage in addition to the primary plan. Secondary insurance — a spouse’s employer plan, Medicaid as secondary to Medicare, a supplemental plan pays after primary adjudication and can cover all or part of the patient’s remaining balance. Capturing secondary insurance at verification ensures the billing workflow triggers secondary billing after primary adjudication is complete, maximizing collection and minimizing the patient balance that must be collected.

Why Verification Must Happen Before Every Visit – Not Just New Patients

The most common insurance verification failure in medical practices is applying the process selectively verifying coverage for new patients thoroughly and assuming established patients’ coverage is unchanged since their last visit. This assumption is statistically incorrect and financially consequential at scale.

Insurance coverage changes at a higher rate than most practices account for. Patients change jobs and health insurance more frequently than in prior decades. Medicaid eligibility is redetermined periodically, and coverage can terminate and reinstate based on income and household changes that the practice has no visibility into. Medicare Advantage open enrollment runs from October 15 to December 7 annually, and patients can switch plans effective January 1. A practice that doesn’t reverify established patient coverage in January risks submitting claims to plans that no longer cover those patients beginning on January 1.

The cost arithmetic strongly favors verification over assumption. A real-time eligibility check takes seconds and costs fractions of a cent in transaction fees. An eligibility denial triggered by unverified coverage change takes three to fourteen days to resolve, consumes billing staff time in investigation and resubmission, and in some cases produces timely filing exposure when the investigation extends close to the new payer’s filing deadline. The return on verification is unambiguous.

The 270/271 Transaction: How Electronic Verification Works

The HIPAA-standard mechanism for electronic insurance verification is the 270/271 transaction pair. The practice’s billing platform or practice management system sends a 270 eligibility inquiry to the payer containing the patient’s member ID, date of birth, and the date of service being verified. The payer processes the inquiry and returns a 271 eligibility response containing the patient’s current coverage status, plan information, deductible and out-of-pocket balance, benefit details, and in some cases authorization requirement flags.

This transaction is faster than phone verification, more accurate than relying on the insurance card the patient presents, and more complete than a manual portal lookup for high-volume practices. Most modern practice management systems support 270/271 transactions and can run batch eligibility checks against the next day’s appointment schedule automatically surfacing coverage issues before the patient arrives rather than at check-in.

The 270/271 transaction is not infallible. Some payers return incomplete benefit information in their 271 response. Some payers’ systems take hours to update after a coverage change, creating a window where an active policy appears terminated or a new plan isn’t yet reflected. For complex benefit questions specific coverage rules for specialty services, authorization criteria, tiered network status the 271 response may need to be supplemented with a direct payer portal lookup or phone call to the payer’s provider services line.

Medicare Advantage: The Verification Complexity Most Practices Underestimate

As of 2025, more than half of Medicare beneficiaries are enrolled in Medicare Advantage plans rather than traditional Medicare. This means that for any practice with significant Medicare patient volume, the majority of those patients are billing to private Medicare Advantage plans rather than to CMS directly and each MA plan has its own coverage rules, prior authorization requirements, in-network provider requirements, and benefit structures that differ from traditional Medicare and from every other MA plan.

The most costly verification failure in practices with Medicare patient populations is failing to identify that a patient has switched from traditional Medicare to a Medicare Advantage plan. A claim submitted to traditional Medicare for a patient enrolled in a Medicare Advantage plan will be denied because traditional Medicare is no longer the primary payer. The practice must then identify the correct MA plan, update billing records, and resubmit to the MA plan, potentially within a compressed timely filing window if the investigation takes time.

The correct verification approach for every Medicare patient is running an eligibility check through the CMS portal or a clearinghouse that returns not just Medicare eligibility but Medicare Advantage enrollment status, including the specific plan. This check must be run before every visit, not just annually, because Medicare Advantage enrollment can change at the start of each calendar year after the annual election period. Related: Verify Medicare Eligibility: What Providers Must Know

Coordination of Benefits: Identifying Primary vs Secondary Coverage

When a patient has more than one insurance plan, the coordination of benefits rules determine which insurer pays first and which pays second. Getting this order wrong produces a claim that is denied by the payer who receives it as primary when they are actually secondary — creating an investigation requirement and resubmission delay that verification would have prevented.

The most common coordination of benefits questions arise in three situations. First, Medicare-employer plan coverage: a Medicare-eligible patient who is still employed and covered by an employer group health plan may have either Medicare or the employer plan as primary depending on the employer’s size. Employers with 20 or more employees maintain primary coverage over Medicare for working employees. Smaller employers’ plans are secondary to Medicare. Getting this wrong generates a primary payer mismatch denial.

Second, Medicare-Medicaid dual eligibility: patients enrolled in both Medicare and Medicaid are dual-eligibles where Medicare is primary and Medicaid is secondary. Claims for dual-eligible patients must first be submitted to Medicare and then to Medicaid for any remaining balance. Submitting to Medicaid first produces a Medicaid denial that refers the claim to Medicare — an avoidable delay.

Third, dependent coverage on two employer plans: a dependent covered by both parents’ employer plans has a coordination of benefits order determined by the birthday rule, the parent whose birthday falls earlier in the calendar year has the primary plan for the dependent. Getting the primary-secondary order wrong produces a denial from whichever insurer receives the claim as primary when they are actually secondary.

What Happens When Verification Fails: The Downstream Billing Consequences

Insurance verification failures don’t just produce eligibility denials. They produce a cascade of downstream billing problems that compound as each one is investigated, corrected, and resolved often weeks after the original encounter.

Eligibility Denials

The immediate consequence of unverified coverage change is an eligibility denial: the claim was submitted to an insurer who is no longer the patient’s active payer, or the patient’s coverage under the submitted plan has lapsed. The denial is not based on whether the service was medically appropriate or correctly coded. It is based on the administrative failure to verify that the insurer on file still covers the patient. Resolving it requires identifying the correct current coverage, updating the billing record, and resubmitting. a process that takes three to fourteen days and consumes billing staff time that wasn’t budgeted for a problem that verification would have prevented in seconds.

Wrong Copay Collection

When verification doesn’t return accurate deductible and benefit information, the front desk collects the wrong patient copay or coinsurance at time of service. If the practice collects less than the patient owes, it has to bill the patient for the remainder after insurance processes, at a much lower collection rate than time-of-service collection. If the practice collects more than the patient owes, it has to issue a refund. Creating administrative overhead and patient dissatisfaction. Both are preventable by collecting accurate benefit information at verification.

Authorization Denials

When verification doesn’t identify that a planned service requires prior authorization under the patient’s plan, the service is delivered without authorization and the claim denies. Related: What Is Health Insurance Pre-Authorization

Authorization denials for services delivered to established patients are among the most common verification-related billing failures because front desks that verify thoroughly for new patient visits often don’t re-verify authorization requirements for established patients who are receiving services they’ve received before. The patient’s plan may have changed, or the plan’s authorization requirements may have changed, and neither is visible without re-verification.

Out-of-Network Billing Disputes

When in-network status isn’t verified at the plan level, patients receive services from providers they believe are in-network based on the payer logo on their card, only to receive a bill reflecting out-of-network cost-sharing that is significantly higher than expected. These situations generate patient complaints, billing disputes, and in some cases requests for waiver of the cost-sharing differential that the practice has no contractual ability to honor. They are entirely preventable by verifying in-network status at the specific plan level before the patient arrives.

Building a Verification Workflow That Works at Volume

The verification process that works for a practice seeing 10 patients per day and the verification process that works for a practice seeing 60 patients per day are structurally different. At low volume, manual verification of each patient by a front desk staff member the morning before the appointment is feasible. At high volume, manual verification becomes the bottleneck that either prevents thorough verification or consumes so much staff time that other functions are deprioritized.

The verification workflow that scales to high volume uses automation as the foundation and human review as the exception handler. The practice management system or billing platform runs 270/271 eligibility checks automatically for every patient on the next day’s schedule — typically in an overnight batch run — and surfaces any patients with coverage issues flagged for manual review the following morning. Staff review only the flagged exceptions rather than running manual checks on every patient.

The automation handles the routine verification efficiently. The staff handles the exceptions — patients with lapsed coverage, patients whose plans have changed, patients with new secondary insurance, patients whose authorization requirements have changed. This split reduces the time per verified patient from two to three minutes of manual effort to seconds of automated processing, with human attention concentrated on the cases that actually require it.

Warning: Automated eligibility verification does not eliminate the need for manual check-in confirmation. The 270/271 transaction queries the payer with the information the practice has on file. If that information is wrong, a transposed member ID, an old plan number, a payer that was updated in the system incorrectly the electronic check returns results based on the wrong query. Confirming the insurance card at check-in for every patient, every visit, catches the discrepancies between what the system has on file and what the patient actually has in their wallet. Both layers are needed.

The At-Check-In Layer: Why the Card Confirmation Still Matters

Automated pre-visit verification covers the eligibility check. It doesn’t cover what the patient brings through the door on the day of the visit. The at-check-in layer is the human verification step that catches what automation cannot: the patient who changed insurance since the automated check was run yesterday, the patient who shows up with a different insurance card than what’s on file, the patient who forgot to mention a new secondary insurance, and the patient who enrolled in a new plan this week that the prior authorization system doesn’t yet have on record.

The at-check-in verification standard is simple: ask every patient at every visit whether their insurance has changed since their last visit, collect and scan the insurance card, compare against the card on file, and update the record if there’s a difference. This takes 30 to 60 seconds per patient. It catches the coverage changes that slip through automated pre-visit checks and prevents the eligibility denials that a missed same-day change would otherwise generate.

For practices where front desk staff have high turnover or inconsistent training, the at-check-in verification question is the most direct improvement lever available. It requires no technology investment. It requires no system configuration. It requires only a consistent practice standard — ask the question, confirm the card, update if changed applied to every patient, every visit, regardless of how long they’ve been a patient.

How Qualigenix Manages Insurance Verification

At Qualigenix, insurance verification is the first step in the claims processing workflow we manage for practices across 38+ specialties. We run automated 270/271 eligibility checks from the appointment schedule for every patient before every visit, flag coverage issues for practice-side resolution before the patient arrives, and maintain the benefit information deductible status, authorization requirements, in-network status that the coding and billing functions downstream depend on.

We manage Medicare Advantage identification as a specific verification step, distinguishing traditional Medicare from MA enrollment and identifying the specific MA plan for every Medicare patient before each visit. We maintain coordination of benefits records for patients with multiple insurance plans and trigger secondary billing automatically after primary adjudication is complete.

Our verification process is integrated with the authorization management function so that when verification surfaces an authorization requirement for a planned service, the authorization workflow initiates immediately before the service is delivered, not after. This integration eliminates the authorization denial category that results from services delivered to patients whose verification was completed but whose authorization requirement wasn’t flagged in time.

Related: What Is RCM in Medical Billing | Denial Management: Common Denials and How to Fix Them | What Is Aging Accounts Receivable

Insurance Verification Readiness Checklist

- Automated 270/271 eligibility checks run for every scheduled patient — not only new patients

- Batch verification runs 24 to 48 hours before each day’s appointments

- Flagged coverage issues reviewed and resolved before patient arrives — not at check-in

- Medicare patients verified for MA enrollment status at every visit through CMS portal or clearinghouse

- In-network status confirmed at plan level — not just payer level

- Prior authorization requirements surfaced at verification — not at claim submission

- Deductible and out-of-pocket status captured for patient responsibility estimation

- Secondary insurance identified and recorded at verification

- At check-in: insurance change question asked of every patient every visit

- Insurance card scanned and compared to record at check-in — updated if different

- Coordination of benefits order confirmed for patients with multiple plans

- Eligibility denial root causes tracked monthly — recurring patterns trigger upstream process fix

Frequently Asked Questions: Insurance Verification

What is insurance verification in healthcare?

Insurance verification is the process of confirming a patient’s coverage is active and determining the specific benefits, in-network status, authorization requirements, and patient financial responsibility applicable to planned services before the encounter. It is the front-end revenue cycle function that determines whether a claim will be paid. When done correctly before every visit, it prevents eligibility denials, wrong copay collection, out-of-network billing surprises, and authorization failures — all of which are more expensive to resolve after the fact than to prevent through verification.

Why must insurance verification happen before every visit?

Insurance coverage changes continuously — patients change employers, switch Medicare Advantage plans, have Medicaid coverage redetermined, and add or drop secondary insurance without notifying the practice. A patient whose coverage was confirmed three months ago may be on a completely different plan today. The cost of an eligibility denial investigation — three to fourteen days of billing staff time — exceeds the cost of a pre-visit eligibility check by a wide margin. Treating established patients as automatically verified is a cost-cutting assumption that produces more costs than it saves.

What does insurance verification confirm?

Complete verification confirms: active coverage status on the date of service, correct payer and plan identification, in-network status for the rendering provider at the specific plan level, prior authorization requirements, deductible and out-of-pocket status, referral requirements, and secondary insurance. Verification that only confirms active coverage — a simple yes/no eligibility check — misses the benefit details, authorization flags, and secondary insurance information that the rest of the billing workflow depends on to process the claim correctly and collect the right patient responsibility.

How does Medicare Advantage complicate insurance verification?

Over 50% of Medicare beneficiaries are now enrolled in Medicare Advantage plans, private insurance that must be billed to the specific MA plan, not to traditional Medicare. A claim submitted to traditional Medicare for an MA patient will be denied. MA plans have their own prior authorization requirements, in-network provider requirements, and benefit structures that differ from traditional Medicare and from each other. Every Medicare patient must be verified for MA enrollment status at every visit, and the specific MA plan must be identified not just that the patient has Medicare coverage in general.

What is the 270/271 transaction in insurance verification?

The 270/271 is the HIPAA-standard electronic transaction for insurance eligibility verification. The practice sends a 270 inquiry with the patient’s member ID and date of service; the payer responds with a 271 containing current coverage status, plan details, and benefit information in real time. Modern practice management systems run 270/271 checks automatically from the appointment schedule. The results are faster and more accurate than phone verification. They don’t replace the at-check-in card confirmation, which catches same-day changes that weren’t reflected in the prior evening’s automated batch check.

What happens when insurance verification is skipped?

When verification is skipped, coverage changes slip through and generate eligibility denials, wrong payer submissions, missing authorization failures, and incorrect patient copay collection all of which require investigation and correction after the fact at a cost that exceeds the verification itself. Eligibility denials take three to fourteen days to resolve and may consume timely filing days at the new payer during the investigation period. Out-of-network billing surprises generate patient disputes. Missing authorization triggers a denial that requires retroactive authorization investigation. Each preventable failure compounds the billing team’s workload on problems that should never have reached the billing queue.

Related Resources from Qualigenix

- What Is RCM in Medical Billing

- Accounts Receivable

- Insurance Authorization for Specialty Practices

- What Is Claim Submission in Medical Billing

- Provider Credentialing Services

Verify Before the Visit. Get Paid After It.

Qualigenix manages insurance verification as the first step in the revenue cycle for practices across 38+ specialties — automated eligibility checks, Medicare Advantage identification, authorization requirement flagging, and secondary insurance capture — so every claim submits with accurate coverage information from the start.

Our team delivers 99% claim accuracy, a 95% first-pass acceptance rate, an average 36-day collection cycle, and a 30% reduction in AR days. We onboard in as few as 6 days.

Precision. Progress. Qualigenix.

What’s Next

Medical Coding Errors That Cost Practices the Most (And How to Catch Them Before They Submit)

Medical Coding Errors That Cost Practices the Most (And How to Catch Them Before They Submit) Written by the...

Insurance Denial Appeals: What Practices Miss

Most insurance denial appeals that fail don’t fail because the clinical case was weak. They fail because the...

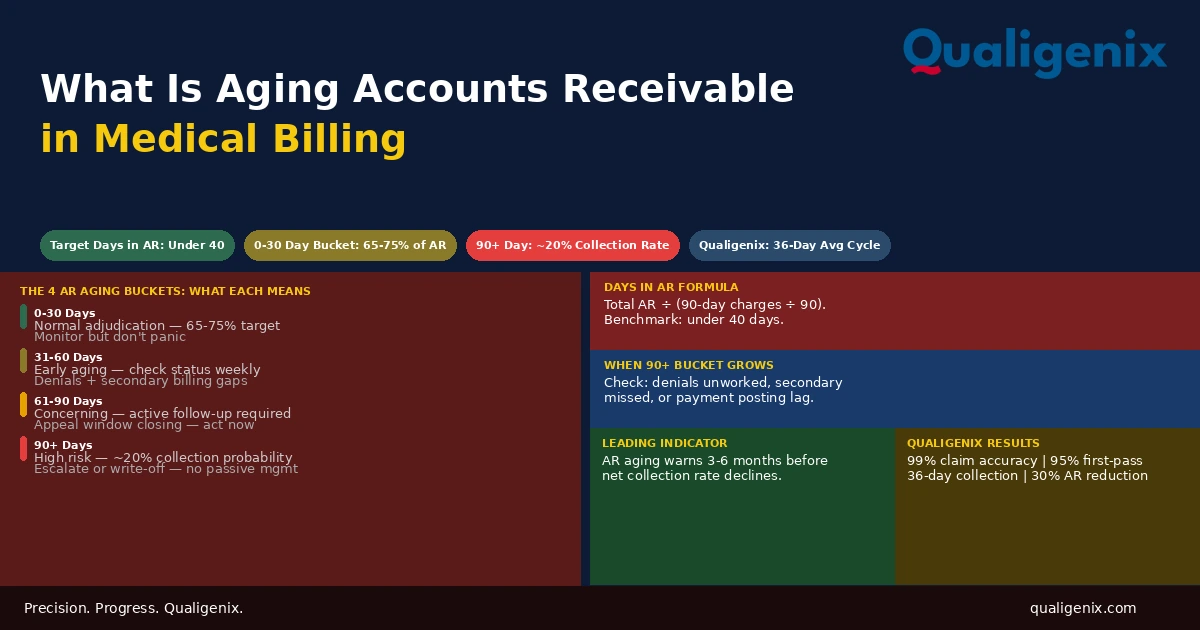

What Is Aging Accounts Receivable in Medical Billing

Aging accounts receivable is the financial picture of revenue owed but not yet collected, organized by how long it...