Medicare Secondary Payer: Rules, Billing Workflow, and Common Mistakes to Avoid

The Qualigenix Editorial Team consists of certified billing and coding experts with over 40 years of experience across 38+ medical specialties. Our content is rigorously researched against CMS, AMA, and payer-specific guidelines to ensure total compliance and accuracy. We apply the same elite standards to our resources as we do our client work, consistently delivering high claim accuracy and significant reductions in AR days.

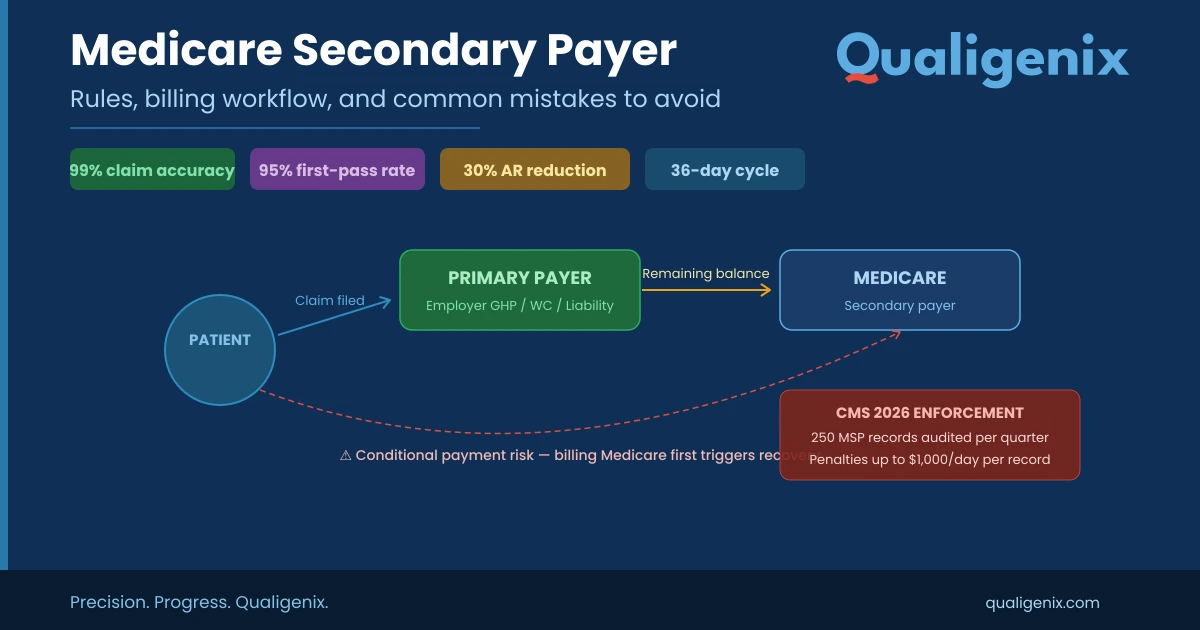

Medicare Secondary Payer (MSP) rules determine which insurer pays first when a Medicare beneficiary has other coverage. Providers must identify the primary payer before submitting claims—billing Medicare first when another insurer is responsible triggers conditional payments, recovery demands, and penalties up to $1,000/day per record. CMS is now auditing 250 MSP records per quarter in 2026. This guide covers every MSP scenario, the correct billing workflow, 7 costly mistakes to avoid, and how Qualigenix’s RCM services protect your revenue.

If your practice treats Medicare beneficiaries—and most do—understanding the Medicare secondary payer (MSP) framework is not optional. It’s the difference between getting paid correctly and chasing down refund demands from CMS months after a claim has closed.

MSP rules govern which insurer pays first when a patient has Medicare alongside another form of coverage. Get the payer order wrong, and your practice faces denied claims, conditional payment recovery notices, and potential civil money penalties. That’s not a hypothetical risk. CMS began auditing 250 MSP records per quarter starting January 2026, and enforcement activity is only accelerating.

This guide breaks down the full Medicare secondary payer landscape for healthcare providers: what the rules say, when Medicare steps back to secondary status, how to bill MSP claims correctly, and the most common mistakes that cost practices real revenue. We’ll also show you how a structured revenue cycle management approach—like the one Qualigenix delivers—can protect your practice from MSP compliance gaps and Medicare coordination of benefits errors.

Let’s start with the fundamentals.

What Is a Medicare Secondary Payer?

Medicare Secondary Payer (MSP) is the federal law that makes Medicare the second payer when a beneficiary has other insurance that must pay first—such as an employer group health plan, workers’ compensation, or liability coverage. MSP ensures Medicare does not cover costs another insurer is legally responsible for (42 U.S.C. § 1395y(b)).

The MSP provisions were introduced in 1980 when Congress expanded Medicare’s coordination of benefits rules beyond workers’ compensation and VA benefits. Since then, MSP has saved Medicare billions annually—roughly $9.7 billion in FY2021 alone, according to CMS data (CMS MSP Savings Report). For providers, Medicare secondary payer compliance means correctly identifying which payer is primary before submitting claims, collecting the right information at registration, and billing in the proper order to avoid payment disruptions.

MSP is sometimes confused with Medicare Supplement (Medigap) insurance, but they serve entirely different functions. We’ll clarify that distinction later in this guide.

Medicare Secondary Payer: Key Stats at a Glance

| Metric | Value |

|---|---|

| MSP savings to Medicare Trust Fund (FY2021) | $9.7 billion (CMS) |

| CMS quarterly MSP audit volume (2026) | 250 records per quarter |

| Civil money penalty for late Section 111 reporting | Up to $1,000 per day per record |

| Reimbursement deadline for conditional payments | 60 days after notice |

| Penalty for failure to reimburse conditional payment | Double the original payment amount |

| ESRD coordination period (GHP pays primary) | 30 months |

| Employer size threshold — working aged (65+) | 20 or more employees |

| Employer size threshold — disabled (under 65) | 100 or more employees |

| Medicare Advantage improper payment rate (estimated) | 6.09% ($23.67 billion) |

| Liability settlement recovery threshold 2026 | $750 (CMS November 2025 alert) |

| Qualigenix claim accuracy rate | 99% |

| Qualigenix first-pass acceptance rate | 95% |

| Qualigenix average collection cycle | 36 days |

| Qualigenix reduction in AR days | 30% |

| Qualigenix average onboarding time | 6 days |

When Does Medicare Become the Secondary Payer?

Medicare doesn’t default to secondary status automatically. Specific conditions must be met based on the type of other coverage the patient carries and the patient’s employment situation. Here are the primary Medicare coordination of benefits scenarios that trigger MSP status.

1. Working Aged Beneficiaries (Age 65+) and Employer Group Health Plans

When a Medicare beneficiary age 65 or older is still working—or has a spouse who is still working—and is covered by an employer group health plan (GHP), that employer plan pays first. The key threshold: the employer must have 20 or more employees (42 U.S.C. § 1395y(b)(1)(A)). If the company has fewer than 20 workers, Medicare remains primary and the GHP becomes secondary.

This scenario catches many practices off guard. A 67-year-old patient walks in with both a Medicare card and an employer insurance card. If that employer has 20+ employees and the patient or their spouse is actively employed, the employer plan is primary—not Medicare. Billing Medicare first in this situation creates a conditional payment that CMS will recover.

2. Disabled Beneficiaries (Under Age 65) with Employer Coverage

Medicare-eligible individuals under 65 who qualify based on disability can also trigger Medicare secondary payer rules. If a disabled beneficiary is covered by an employer GHP through their own current employment, a spouse’s employment, or a parent’s employment, the GHP pays first. The employer size threshold jumps to 100 or more employees—double the threshold for working aged individuals (42 U.S.C. § 1395y(b)(1)(B)).

3. End-Stage Renal Disease (ESRD) and the 30-Month Coordination Period

Patients who qualify for Medicare based solely on an ESRD diagnosis have a unique coordination window. Any group health plan coverage they carry through an employer is primary for the first 30 months of Medicare eligibility (per CMS MSP Manual). After those 30 months, Medicare flips to primary. This 30-month coordination period applies regardless of employer size or current employment status—a notable exception to the standard MSP rules.

4. Workers’ Compensation Claims

When a patient’s medical treatment is related to a workplace injury or illness, workers’ compensation pays first. This has been true since Medicare’s creation in 1965. If the workers’ comp claim is contested, Medicare may step in with a conditional payment to ensure the beneficiary still receives care, but that payment must be reimbursed once the claim resolves.

5. Liability Insurance and No-Fault Auto Coverage

Auto accidents, slip-and-fall incidents, and other liability situations trigger MSP rules as well. The at-fault party’s liability insurer or the patient’s no-fault auto coverage pays primary. Medicare may make conditional payments if the liable insurer delays, but expects full reimbursement once a settlement or judgment occurs. The 2026 recovery threshold for physical trauma-based liability settlements remains at $750 (per CMS November 2025 alert).

Who Pays First? MSP Quick-Reference Table

Use this Medicare coordination of benefits table to quickly determine primary vs. secondary payer status:

| Patient Scenario | Primary Payer | Secondary Payer | Key Condition / Rule |

|---|---|---|---|

| Age 65+, actively employed, GHP coverage | Employer GHP | Medicare | Employer has 20+ employees |

| Age 65+, retired, has retiree GHP | Medicare | Retiree GHP | Not currently employed |

| Under 65, disabled, employer GHP | Employer GHP | Medicare | Employer has 100+ employees |

| ESRD patient, first 30 months | Employer GHP | Medicare | 30-month coordination period |

| ESRD patient, after 30 months | Medicare | Employer GHP | Coordination period ended |

| Work-related injury | Workers’ Comp | Medicare (conditional) | Injury tied to employment |

| Auto accident / liability claim | Liability / No-Fault Insurer | Medicare (conditional) | Third-party responsible |

| Age 65+, COBRA coverage | Medicare | COBRA | COBRA always secondary for 65+ |

| ESRD + COBRA, first 30 months | COBRA | Medicare | ESRD coordination period active |

| VA coverage | Bill one or the other | Not MSP | VA and Medicare do not coordinate under MSP |

Pro tip: Always verify coverage at every visit. A patient’s employment status and insurance lineup can change between appointments, flipping the primary/secondary designation overnight.

What Is the Difference Between MSP and Medigap?

Providers and patients frequently confuse Medicare Secondary Payer rules with Medicare Supplement (Medigap) policies. They serve completely different functions in the payment process.

| Factor | Medicare Secondary Payer (MSP) | Medigap (Medicare Supplement) |

|---|---|---|

| What it is | Federal law determining payer order when a beneficiary has other insurance | Private insurance policy that supplements Original Medicare |

| Who pays first | Another insurer pays primary; Medicare pays secondary | Medicare pays primary; Medigap covers remaining costs |

| When it applies | When employer GHP, workers’ comp, liability, or no-fault coverage exists | When the beneficiary purchases a standalone Medigap policy |

| Provider impact | Must bill primary payer first, then Medicare; wrong order triggers recovery | Bill Medicare as primary; Medigap crossover is often automatic |

| Regulatory basis | 42 U.S.C. § 1395y(b); CMS MSP Manual | Standardized under federal Medigap rules (Plans A–N) |

The distinction matters for billing teams. An MSP situation requires you to identify and bill the primary payer before submitting to Medicare. A Medigap situation follows standard Medicare-primary billing with automatic crossover in most cases. Confusing the two leads to claim rejections and delayed payments.

How Does Medicare Secondary Payer Billing Work? Step-by-Step Workflow

Secondary insurance billing under MSP rules follows a sequential process. Skip a step, and you’re looking at denials, refund demands, or both. Here’s the Medicare coordination of benefits billing workflow from registration to payment.

Step 1: Collect and Verify Coverage at Registration

Before any service is rendered, your front desk or intake team needs to identify every active insurance the patient carries. This means asking about employer coverage, spouse’s employer coverage, workers’ compensation claims, auto accident involvement, and any pending liability cases. CMS requires providers to determine primary vs. secondary payer status before submitting claims (per CMS MSP Manual, Chapter 3).

This is where many practices fall short. A quick scan of the Medicare card and a copy of the insurance card isn’t enough. You need to ask specific MSP-related questions: Is the patient or their spouse currently employed? How many employees does the company have? Is there an open workers’ comp or auto claim? Does the patient have ESRD, and if so, when did Medicare eligibility begin?

At Qualigenix, our insurance eligibility verification process is built to catch MSP scenarios before claims go out the door. Our team verifies not just eligibility but coordination of benefits status, reducing the risk of billing the wrong payer from day one.

Step 2: Bill the Primary Payer First

Once you’ve identified the primary payer, submit the claim there first. Wait for the primary payer’s Explanation of Benefits (EOB) or Remittance Advice (RA) before billing Medicare as secondary. Jumping ahead and billing Medicare first when another payer is primary is one of the fastest ways to trigger a conditional payment situation—and a recovery demand later.

Step 3: Submit the MSP Claim to Medicare with Primary Payer Data

After the primary payer processes the claim, submit the remaining balance to Medicare with the primary payer’s payment information attached. Use the CMS-1500 or CMS-1450 form (or their electronic equivalents) and complete all MSP information fields. This includes the primary payer’s payment amount, adjustment codes, and the EOB/RA data.

Medicare calculates its secondary payment using specific formulas that factor in the primary payer’s allowed amount, the patient’s deductible, and coinsurance obligations (Medicare Secondary Payer Manual, Chapter 5, Section 40.8.3).

Step 4: Post Payments Accurately and Reconcile Multi-Payer Balances

Once both payers have processed the claim, post payments accurately and reconcile any patient responsibility. Errors at this stage—like posting the wrong payer’s payment to the wrong line—create downstream AR headaches that compound over time.

Qualigenix’s payment posting services are designed specifically for multi-payer scenarios like MSP claims. Every payment is matched to the correct payer, the correct claim, and the correct patient balance—so your AR stays clean and your revenue stays on track.

What Are Medicare Conditional Payments and Why Should Providers Care?

A Medicare conditional payment occurs when Medicare pays a claim even though another insurer is the primary payer. Medicare steps in to prevent gaps in beneficiary coverage, but the payment must be reimbursed within 60 days once the primary payer’s responsibility is established. Failure to reimburse can result in double damages (42 U.S.C. § 1395y(b)(2)(B)).

Once the primary payer makes payment—or a settlement, judgment, or award occurs—Medicare expects full reimbursement of its conditional payment. The primary payer, the provider who received funds, the beneficiary, or even the beneficiary’s attorney can be held liable for repayment. Miss the 60-day window, and CMS can pursue double the original payment amount as a penalty.

The Benefits Coordination & Recovery Center (BCRC) manages conditional payment recovery for non-group health plan situations (liability, no-fault, workers’ comp), while the Coordination of Benefits Contractor (COBC) handles GHP-related coordination. Both entities have become increasingly aggressive in their recovery efforts, and CMS’s 2026 enforcement ramp-up only intensifies the urgency.

For providers, the takeaway is straightforward: if you bill Medicare as primary when it should have been secondary, expect a recovery letter. And if you can’t demonstrate that you took reasonable steps to identify the correct primary payer, the liability falls squarely on your practice.

How Long Does Medicare Have to Recover Conditional Payments?

There is no specific statute of limitations on Medicare’s right to recover conditional payments from beneficiaries or providers for GHP situations. For Section 111 reporting-related penalties, CMS follows a 5-year statute of limitations from the date of noncompliance. However, for conditional payment recovery itself, Medicare can pursue recovery at any point after the primary payer’s obligation is established.

The practical implication: old claims can resurface years later if CMS identifies an MSP discrepancy. This is not a theoretical risk—it is an active enforcement reality in 2026.

Can Medicare Pursue Recovery from Providers Directly?

Yes. Federal law allows Medicare to recover conditional payments from any entity that received the funds, including providers, suppliers, beneficiaries, and attorneys (42 U.S.C. § 1395y(b)(2)(B)(iii)). If your practice received a Medicare primary payment that should have been secondary, CMS can and will send a recovery demand directly to you.

What Are the MSP Compliance Requirements for Section 111 Reporting?

Section 111 of the Medicare, Medicaid, and SCHIP Extension Act of 2007 (MMSEA) requires insurers, self-insured entities, and group health plans to report specific claims data to CMS. This reporting enables CMS to identify Medicare secondary payer situations and coordinate benefits properly. While the direct reporting obligation falls on Responsible Reporting Entities (RREs)—typically insurers and self-insured employers—the downstream impact on providers is significant.

When an RRE reports that a patient has primary coverage through a group health plan, CMS updates the beneficiary’s Medicare eligibility file. If your practice then submits a claim to Medicare as primary without acknowledging that existing MSP record, the claim gets flagged, denied, or conditionally paid.

CMS finalized civil money penalty regulations in October 2023 (effective October 2024), establishing penalties for RREs that fail to report within 365 days of the later of the coverage effective date or the beneficiary’s Medicare entitlement date. Starting in January 2026, CMS is auditing 250 MSP records per quarter to enforce compliance. Penalties can exceed $1,000 per day per unreported record. While these penalties target insurers directly, the ripple effect of inaccurate eligibility files, unexpected claim denials, and retroactive payment adjustments hits your revenue cycle hard.

What Are the Most Common Medicare Secondary Payer Billing Mistakes?

These are the MSP billing and process errors we see most frequently in practices across the country. Each one costs real revenue.

Mistake 1: Failing to Ask MSP-Specific Questions at Registration

Simply copying insurance cards at check-in is not MSP compliance. Your intake process must include direct questions about current employment status, employer size, spouse’s employment, and any active injury or liability claims. Without these answers, your team is guessing at payer order—and guessing wrong means conditional payments, denials, and recovery demands.

Mistake 2: Billing Medicare as Primary Without Verifying COB Status

When front-desk staff skip eligibility verification or rely on outdated information, claims go to Medicare first when they shouldn’t. This creates conditional payments and triggers recovery activity that disrupts cash flow months down the line. Real-time coordination of benefits verification eliminates this risk.

Mistake 3: Submitting MSP Claims Without the Primary Payer’s EOB

Medicare needs the primary payer’s payment data to calculate its secondary payment correctly. Submit claims without the EOB or RA, and you’ll get a denial or a Secondary Claim Development Questionnaire that delays payment by weeks.

Mistake 4: Ignoring the 30-Month ESRD Coordination Period

The ESRD coordination window is one of the trickiest MSP rules. Billing teams that don’t track the 30-month window bill Medicare as primary too early (or too late), creating payment errors in both directions. Track ESRD eligibility dates in your billing system and flag the 30-month transition automatically.

Mistake 5: Missing Employment Status Changes Between Visits

A patient retires, and suddenly Medicare flips from secondary to primary. A spouse loses a job, and the employer GHP drops off. If your team doesn’t catch that change at the next visit, claims go to the wrong payer. Re-verification at each appointment is non-negotiable under MSP rules.

Mistake 6: Skipping No-Pay Bills for Fully Covered MSP Claims

Even when the primary payer covers a claim in full, you still need to submit the claim to Medicare. No-pay bills update benefit period tracking, satisfy frequency limitations, and credit unmet deductibles. Skipping this step creates problems on future claims that ripple through the patient’s Medicare record.

Mistake 7: Not Monitoring Conditional Payments on Liability Cases

When a liability or workers’ compensation case involves a Medicare beneficiary, conditional payments accumulate over the life of the case. Practices that don’t track these conditional amounts face unexpected recovery demands—sometimes for substantial sums—when the case settles. Use your billing system or RCM partner to flag and monitor these cases proactively.

How Is MSP Enforcement Changing in 2026?

The Medicare secondary payer enforcement landscape has shifted dramatically. Here are the developments providers and billing teams need to prepare for:

- CMS quarterly audits now active: CMS began auditing 250 MSP records per quarter in January 2026 (per CMS enforcement guidance). This marks a significant ramp-up from historical enforcement levels and signals a move from passive monitoring to active compliance oversight.

- Civil money penalties fully enforced: The October 2023 final rule on MSP civil money penalties (applicable since October 2024) is now in full effect. RREs that fail to report coverage information within 365 days face per-day penalties. As enforcement matures, the downstream impact on provider claims—inaccurate eligibility files, unexpected denials, retroactive adjustments—is growing.

- Private recovery entities escalating: Organizations like MSP Recovery LLC have built their business model around pursuing double damages for alleged conditional payment violations. Their demand letters and litigation activity are increasing, often using data-mining techniques to identify potential recovery targets.

- Medicare Advantage plans pursuing recovery: CMS has signaled that Medicare Advantage (Part C) and Prescription Drug (Part D) plans should pursue their own conditional payment recoveries more aggressively. Expect increased data sharing between CMS and MA plans, and more conditional payment letters from MA organizations throughout 2026.

- Non-submit MSAs gaining acceptance: Non-submit Medicare Set-Aside (MSA) allocations are becoming a mainstream compliance strategy, particularly for workers’ compensation settlements. CMS’s workload review thresholds have never been “safe harbors,” and the industry is shifting toward risk-based MSA analysis rather than threshold-driven approaches.

For providers, the compliance cost of getting Medicare secondary payer rules wrong has never been higher. Proactive verification, clean billing workflows, and airtight documentation are your best defences.

How Does Qualigenix Protect Your Practice from MSP Revenue Leakage?

Medicare secondary payer compliance isn’t a one-person job. It touches registration, eligibility verification, coding, claim submission, payment posting, and AR follow-up. That’s why practices across 38+ specialties trust Qualigenix to manage the entire revenue cycle—MSP complexities included.

Here’s what our end-to-end RCM approach means for MSP compliance:

- Eligibility verification with COB check: Our team verifies not just patient eligibility but coordination of benefits status before every claim, catching Medicare secondary payer scenarios early. Learn more about our insurance eligibility verification services.

- 99% claim accuracy on MSP claims: Our coding and billing teams are trained on MSP-specific billing rules, including correct form completion, EOB attachment, payer sequencing, and condition code usage.

- Proactive denial management: When MSP-related denials do occur, our denial management team resolves them quickly, identifying root causes, correcting claims, and resubmitting within payer timelines.

- AR follow-up on multi-payer claims: MSP claims involve multiple payers and longer payment cycles. Our AR follow-up services track every claim through the full payment lifecycle, including conditional payment monitoring.

- 95% first-pass acceptance rate: Our clients see measurable improvements in collection speed, with a 36-day average collection cycle and a 30% reduction in AR days.

- 6-day average onboarding: We start with a comprehensive AR assessment that identifies where revenue is stuck—including MSP gaps—and can have your account fully operational within days.

MSP Billing Compliance Checklist for Healthcare Providers

Use this checklist to audit your current Medicare secondary payer workflow:

- ☐ MSP intake questions: Patient intake form includes questions on current employment, employer size, spouse employment, and active injury or liability claims

- ☐ COB verification at every visit: Staff verifies coordination of benefits status at each appointment—not just the first visit

- ☐ Primary payer billed first: Primary payer is identified and billed first for every MSP-eligible patient before submitting to Medicare

- ☐ EOB/RA attached: Primary payer’s Explanation of Benefits or Remittance Advice is attached when billing Medicare as secondary

- ☐ MSP fields completed: All MSP-specific fields on CMS-1500 and CMS-1450 forms are completed accurately

- ☐ No-pay bills submitted: No-pay claims are submitted to Medicare when the primary payer covers the claim in full

- ☐ ESRD tracking active: ESRD patients are tracked for the 30-month coordination period with automated transition alerts

- ☐ Conditional payments flagged: Conditional payments are monitored and flagged in the billing system for recovery tracking

- ☐ Status changes captured: Employment and insurance status changes are verified and documented at each patient visit

- ☐ Annual MSP training: Billing staff receive annual MSP compliance training covering rule updates and payer-specific requirements

Frequently Asked Questions About Medicare Secondary Payer

What triggers Medicare secondary payer status?

MSP status is triggered when a Medicare beneficiary has another form of coverage legally required to pay first. Common triggers include employer group health plans (for working aged 65+ or disabled beneficiaries), workers’ compensation claims, liability insurance, and no-fault auto coverage. Employer size and employment status determine which rules apply.

The specific thresholds are 20+ employees for working aged beneficiaries and 100+ employees for disabled beneficiaries. ESRD patients have a 30-month coordination period regardless of employer size. Each scenario has distinct billing requirements that your team must follow to avoid payment errors.

What happens if a provider bills Medicare as primary by mistake?

Medicare may process the claim as a conditional payment, then seek reimbursement once the correct primary payer is identified. The provider receives a recovery demand letter requiring repayment within 60 days. Failure to reimburse can result in CMS pursuing double the original payment amount as a penalty.

To prevent this, verify coordination of benefits status before every claim submission. If a conditional payment has already been made, work with the BCRC or COBC to resolve the recovery before penalties escalate.

How does the 30-month ESRD coordination period work?

When a patient qualifies for Medicare solely based on end-stage renal disease, any employer group health plan coverage pays primary for the first 30 months of Medicare eligibility. After 30 months, Medicare becomes primary. This applies regardless of employer size or employment status.

Track the ESRD eligibility start date in your billing system and set automated alerts for the 30-month transition. Billing the wrong payer during or after this window is one of the most common MSP errors.

Is COBRA coverage primary or secondary to Medicare?

For beneficiaries age 65 or older, Medicare is primary and COBRA is secondary. For ESRD-eligible beneficiaries in the first 30 months of their coordination period, COBRA pays primary. The payer order depends on the qualifying event and the beneficiary’s Medicare eligibility category.

What is a Medicare conditional payment?

A conditional payment is when Medicare pays a claim even though another insurer is the primary payer. Medicare makes these payments to ensure beneficiaries receive timely care. The payment must be reimbursed within 60 days once the primary payer’s obligation is established. The BCRC manages recovery for liability, no-fault, and workers’ comp cases.

How can providers avoid MSP-related claim denials?

Start with thorough eligibility and COB verification at every patient visit. Train front desk staff to ask MSP-specific questions. Bill the primary payer first, attach the EOB when submitting to Medicare, track ESRD coordination periods, and submit no-pay bills when the primary payer covers claims in full.

Working with an RCM partner like Qualigenix automates many of these steps and reduces human error. Our team catches MSP scenarios during pre-claim verification, preventing denials before they happen.

What is the difference between MSP and Medigap?

MSP is a federal law that determines payer order when a beneficiary has other insurance. Medigap is a private supplemental policy that covers costs left after Medicare pays as primary. MSP requires billing the other insurer first; Medigap kicks in after Medicare has already paid its share. They operate independently.

Related Qualigenix Resources

Explore more guides and services to strengthen your revenue cycle and MSP compliance:

Service Pages:

- Insurance Eligibility Verification Services

- Denial Management Services

- Payment Posting Services

- AR Follow-Up Services

- Revenue Cycle Management Services

Blog Guides:

- The Importance of Eligibility Checks and Benefit Verification in RCM

- How to Appeal an Insurance Claim Denial Step by Step

- Healthcare Billing Process Explained: End-to-End Workflow

- What Is Revenue Cycle Management? A Beginner’s Guide

- How to Reduce Medical Claim Denials: Your 2025 Guide

- Patient Eligibility Verification: Workflow, Tools & ROI for 2026

- Home Health Billing Guidelines Complete Compliance Guide 2026

Stop Losing Revenue to MSP Billing Errors — Book a Free Consultation

Medicare secondary payer rules are complex, CMS enforcement is tightening, and the financial consequences of non-compliance are growing every quarter. Whether your practice struggles with payer identification, conditional payment tracking, or MSP-related denials, Qualigenix has the expertise and infrastructure to fix it.

Our team delivers 99% claim accuracy, a 95% first-pass acceptance rate, and an average 36-day collection cycle. We onboard in as few as 6 days, starting with a comprehensive AR assessment that identifies where revenue is stuck—including MSP gaps.

Precision. Progress. Qualigenix.

What’s Next

Appeal or Write Off? A Decision Framework for Denied Claims Over $500

Don’t let the dollar amount make the call by itself. Sort the denial by reason code, run the...

Switching RCM Vendors Mid-Contract: What Actually Breaks During the Handoff

Switching RCM vendors before a contract ends feels like the fast fix for a billing team that’s underperforming....

Medical Coding Errors That Cost Practices the Most (And How to Catch Them Before They Submit)

Medical Coding Errors That Cost Practices the Most (And How to Catch Them Before They Submit) Written by the...