Medicare Sequestration 2026: What It Means for Your Practice Revenue

The Qualigenix Editorial Team consists of certified billing and coding experts with over 40 years of experience across 38+ medical specialties. Our content is rigorously researched against CMS, AMA, and payer-specific guidelines to ensure total compliance and accuracy. We apply the same elite standards to our resources as we do our client work, consistently delivering high claim accuracy and significant reductions in AR days.

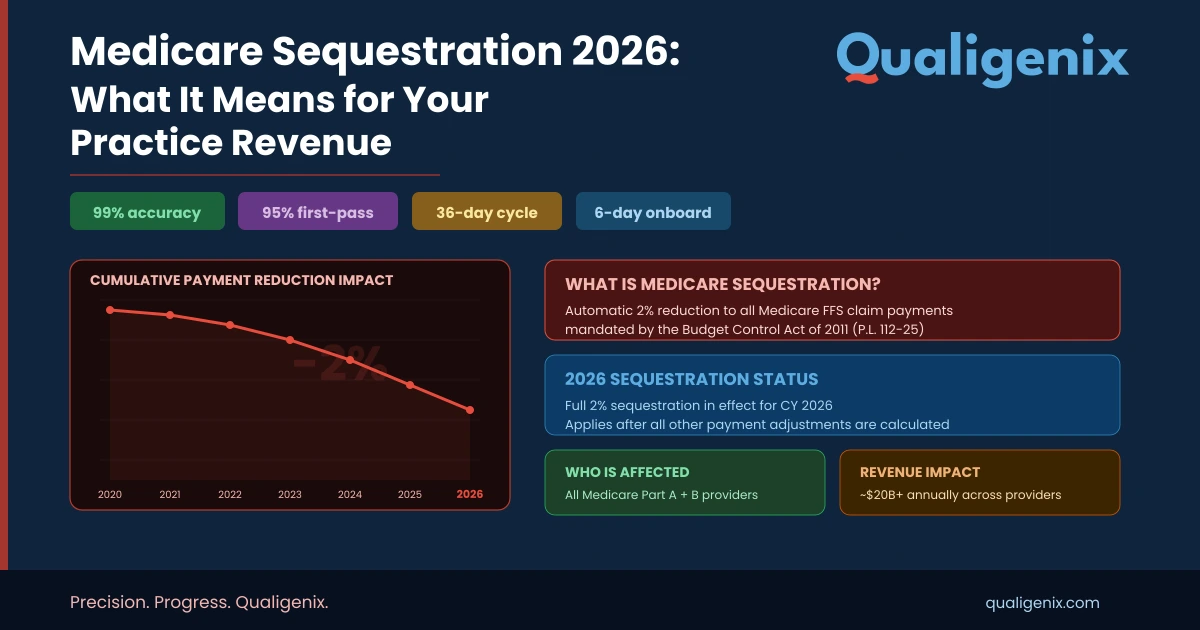

| Summary Medicare sequestration is a mandatory across-the-board reduction in Medicare payments to providers, driven by two separate federal budget enforcement laws. The Budget Control Act (BCA) of 2011 imposes a permanent 2% cut on all Medicare Part A and Part B claims, applied after adjudication and extended through February 2033. A second potential cut — a 4% PAYGO reduction triggered by the One Big Beautiful Bill Act — was waived by Congress in November 2025. The 2% BCA cut remains active in 2026. Understanding how sequestration affects your remittance, your AR forecasting, and your revenue cycle strategy is non-negotiable for every practice billing Medicare. |

What Is Medicare Sequestration?

| Medicare sequestration is a mandatory federal budget enforcement mechanism that automatically reduces Medicare payments to healthcare providers by a fixed percentage. Under the Budget Control Act of 2011, a 2% reduction applies to all Medicare Part A and Part B fee-for-service claims with dates of service on or after April 1, 2013. The reduction is applied post-adjudication — after Medicare calculates the allowed amount and after patient coinsurance and deductibles are determined — and does not affect beneficiary out-of-pocket costs. The 2% BCA sequestration remains in effect through February 28, 2033. |

Sequestration sounds abstract. The billing impact is not. Every time Medicare processes a claim and calculates your allowed amount, a 2% reduction is applied before the check is cut. On a single claim for a $1,000 service, that is $20 taken off the top. For a practice billing $5 million annually in Medicare, that is $100,000 removed from your revenue each year — automatically, with no action required by CMS and no opportunity for you to appeal the reduction itself.

That math has been playing out since April 1, 2013, when sequestration first took effect under the Budget Control Act of 2011. It will continue through February 28, 2033, under current law. And in late 2025, the Medicare sequestration picture got dramatically more complicated when the passage of the One Big Beautiful Bill Act triggered the Statutory Pay-As-You-Go (PAYGO) mechanism — threatening an additional 4% reduction on top of the existing 2%, for a combined 6% cut.

Congress intervened. A stopgap spending bill signed November 12, 2025 waived the PAYGO sequestration for 2026. The immediate threat was neutralized. But the structural risk has not disappeared — it will resurface with any future legislation that increases the federal deficit without offsetting spending. For practices billing significant Medicare volumes, understanding sequestration mechanics is not optional background knowledge. It is active revenue cycle management.

2026 Medicare Sequestration — Key Stats at a Glance

| Metric | Value / Detail |

| Current BCA Sequestration Rate (2026) | 2% — applied to all Medicare Part A and Part B FFS claims |

| BCA Sequestration Active Since | April 1, 2013 |

| BCA Sequestration Extended Through | February 28, 2033 |

| Potential PAYGO Sequestration (2026 Risk) | 4% — WAIVED by Congress on November 12, 2025 |

| Would-Be Combined Cut (If PAYGO Not Waived) | 6% total (2% BCA + 4% PAYGO) |

| PAYGO Medicare Cut Cap (by law) | 4% maximum |

| Revenue Impact: $5M Medicare Practice | $100,000/year at 2% sequestration |

| Remittance Claim Adjustment Code | CARC 253 — identifies sequestration reduction on EOB |

| Does It Affect Beneficiary Cost Sharing? | No — patient deductibles and coinsurance are unaffected |

| Does It Affect Medicare Advantage Plans? | Yes — capitation payments to MA plans are reduced |

| Qualigenix AR Days Reduction | 30% average |

| Qualigenix Clean Claim Accuracy | 99% |

How Does Medicare Sequestration Actually Work in Billing?

Sequestration does not change your fee schedule rates. It does not alter RVUs or conversion factors. It is applied as a final, post-adjudication adjustment to the Medicare payment amount — meaning it comes after every other calculation has been completed.

Here is the exact order of operations on a Medicare claim:

- CMS adjudicates the claim: The claim is processed against the applicable fee schedule (PFS, OPPS, IPPS, etc.) to determine the Medicare allowed amount.

- Beneficiary cost sharing is determined: Patient deductible and coinsurance amounts are identified and applied. These amounts are not affected by sequestration.

- Sequestration is applied: The 2% reduction is applied to Medicare’s remaining payment responsibility — not to the total allowed amount.

- Payment is issued: The check or EFT is issued to the provider for the reduced amount.

The practical example: A service has a Medicare allowed amount of $1,000. The beneficiary owes $200 in coinsurance (20%). Medicare’s share is $800. Apply the 2% BCA sequestration to $800: the deduction is $16. Your actual payment is $784, not $800.

On your Explanation of Benefits (EOB) or Electronic Remittance Advice (ERA), sequestration appears as Claim Adjustment Reason Code (CARC) 253. If you are not seeing CARC 253 on Medicare remittances, your billing team needs to audit whether sequestration is being applied and whether your revenue cycle system is accounting for it correctly in payment posting.

Does Sequestration Apply to All Medicare Claims?

The 2% BCA sequestration applies to Medicare fee-for-service Part A and Part B claims, including professional services (PFS), outpatient hospital (OPPS), inpatient hospital (IPPS), skilled nursing facility (SNF), and home health claims. Medicare Advantage capitation payments to plans are also reduced by sequestration, though the reduction mechanism is different for MA versus FFS.

Sequestration does not apply to Medicaid, private commercial insurance, or Medicare Part D low-income subsidy payments. The PAYGO Act explicitly excludes Medicare Part D catastrophic subsidy payments and the Qualifying Individual Program (which helps low-income beneficiaries pay Part B premiums).

What Is the Difference Between BCA Sequestration and PAYGO Sequestration?

| Factor | BCA Sequestration | PAYGO Sequestration |

| Authorizing Law | Budget Control Act of 2011 | Statutory Pay-As-You-Go Act of 2010 |

| Current Status (2026) | Active — 2% cut in effect | Waived for 2026 (Nov 12, 2025 stopgap bill) |

| Medicare Cut Rate | 2% (statutory cap) | Up to 4% (statutory cap for Medicare) |

| Trigger Mechanism | Triggered by federal deficit levels exceeding BCA thresholds | Triggered when new legislation increases the deficit without offsets |

| Has It Ever Not Been Waived? | No — has been active since 2013 without Congressional waiver | Never taken effect — always waived before activation |

| Duration if Activated | Through February 28, 2033 (current law) | Annual — would continue until Congress offsets or waives |

| Impact on MA Plans | Yes — capitation payments reduced | Yes — would also reduce MA capitation payments |

| Affect on Beneficiary Cost Sharing | No | No |

The 2025 PAYGO Near-Miss: What Happened and What It Means Going Forward

In the summer of 2025, Congress passed the One Big Beautiful Bill Act (OBBBA, H.R. 1). The Congressional Budget Office estimated this legislation would increase the federal deficit by approximately $415 billion in fiscal year 2026 alone. Under the Statutory PAYGO Act, any legislation that increases the deficit triggers automatic sequestration unless Congress acts to waive it or offset the costs.

By law, the Medicare PAYGO cut is capped at 4%. The CBO estimated that a 4% Medicare sequestration would reduce Medicare spending by approximately $45 billion in fiscal year 2026. That is not a rounding error — that is an enormous reduction across every provider setting.

The PAYGO cut had never actually taken effect before. Every prior time a budget bill triggered PAYGO — and there have been multiple instances — Congress passed supplemental legislation to waive the cuts. The November 2025 stopgap bill did exactly that, using the cleared scorecard method to prevent the PAYGO sequestration from activating.

But the structural risk has not been resolved. OMB has estimated that the OBBBA and related fiscal policies will generate deficit increases averaging $230 billion per year between 2026 and 2034. That means PAYGO will be triggered annually unless Congress continues to waive it or passes permanent offsets. The AHA, AMA, and state hospital associations have all called for permanent PAYGO sequestration protection for Medicare providers. Until that legislation passes, the 4% PAYGO threat re-emerges every budget cycle.

How Should Practices Plan for Future PAYGO Sequestration Risk?

The answer is not to assume Congressional action will always come through. The PAYGO waiver passed in November 2025, but the political environment is changing, and future waivers will face steeper partisan challenges. A well-run revenue cycle should be modeled around worst-case scenarios. For practices with high Medicare payer mix, a 4% PAYGO activation on top of the existing 2% BCA cut would represent a 6% haircut on Medicare revenue — a material impact requiring immediate AR management response.

Your RCM strategy should include scenario modeling for sequestration rates at 2%, 4%, and 6%. Understanding the revenue impact of each scenario for your specific payer mix allows you to make informed decisions about Medicare participation, payer contract negotiations with commercial insurers, and operational cost management.

How Does Medicare Sequestration Impact Your Revenue Cycle?

Sequestration creates several distinct challenges across the revenue cycle that require active management:

Payment Posting Accuracy

CARC 253 on your remittance advice is the sequestration flag. If your billing system or payment posting team is not identifying and correctly applying this adjustment code, your accounts receivable will show phantom balances — amounts that appear outstanding but are actually the sequestration deduction Medicare has already accounted for. Confusing sequestration adjustments with genuine underpayments leads to wasted follow-up effort and inflated AR aging reports.

Revenue Forecasting and Budget Modeling

Every Medicare revenue projection your practice builds must incorporate the 2% BCA sequestration. A practice that models Medicare reimbursement based on raw fee schedule allowed amounts — without applying sequestration — will systematically over-project revenue. At scale, this creates budget shortfalls that look like billing performance problems but are actually modeling errors.

AR Follow-Up Prioritization

Sequestration-adjusted payments are not underpayments. They are the correct payment amount under current law. AR follow-up teams that chase sequestration adjustments as underpayments waste resources and generate provider relations friction with Medicare without any prospect of recovery. Your billing system configuration should distinguish CARC 253 adjustments from actual underpayment scenarios requiring appeal.

Payer Mix Strategy

Sequestration affects only Medicare FFS claims — not commercial insurance, not Medicaid (directly), not Medicare Advantage on the provider side. Practices with heavy Medicare payer mix absorb a disproportionate financial burden from sequestration. Understanding payer mix and its interaction with sequestration is a core input for any strategic decision about Medicare participation, panel size, or referral patterns.

Sequestration Revenue Impact Calculator

Use this framework to estimate the annual financial impact of sequestration on your practice:

| Annual Medicare Revenue | 2% BCA Cut | Net After BCA | 6% Combined Cut (BCA + PAYGO) | Net After Combined Cut |

| $1,000,000 | $20,000 | $980,000 | $60,000 | $940,000 |

| $2,500,000 | $50,000 | $2,450,000 | $150,000 | $2,350,000 |

| $5,000,000 | $100,000 | $4,900,000 | $300,000 | $4,700,000 |

| $10,000,000 | $200,000 | $9,800,000 | $600,000 | $9,400,000 |

| $20,000,000 | $400,000 | $19,600,000 | $1,200,000 | $18,800,000 |

10 RCM Strategies to Protect Revenue From Medicare Sequestration

- Model sequestration into every Medicare revenue projection: Use post-sequestration allowed amounts — not raw fee schedule values — as your baseline in financial forecasting.

- Configure CARC 253 correctly in your billing system: Ensure CARC 253 is mapped as a contractual adjustment, not an open AR balance requiring follow-up.

- Run payer mix analysis quarterly: Identify your Medicare FFS exposure as a percentage of total revenue to understand sequestration’s aggregate impact.

- Optimize commercial payer rates to offset Medicare reductions: Strong commercial contract negotiation can compensate for the margin lost to Medicare sequestration.

- Maximize clean claim rates: Every denied or delayed claim amplifies the sequestration burden. A 99% first-pass acceptance rate means you collect your post-sequestration payment on the first submission, every time.

- Monitor QPP performance: Quality Payment Program bonuses can partially offset sequestration-related payment reductions for eligible providers.

- Track PAYGO legislative developments: Assign responsibility in your administrative team for monitoring Congressional action on PAYGO waivers and future sequestration risks.

- Audit payment posting for sequestration accuracy: Periodically verify that CARC 253 adjustments are being applied correctly and consistently across all Medicare remittances.

- Build scenario models for 2%, 4%, and 6% sequestration: Have contingency plans ready for activation if PAYGO sequestration is triggered in a future budget cycle.

- Partner with a proactive RCM company: Qualigenix actively monitors sequestration policy changes and adjusts client billing systems before they create payment posting errors or AR distortions.

How Qualigenix Protects Your Practice From Sequestration Revenue Loss

Sequestration is a policy reality that every Medicare-billing practice must manage. The 2% BCA cut is not going away before 2033. The PAYGO risk re-emerges with every major budget cycle. The only variable you can control is how well your revenue cycle is configured to absorb these reductions without creating downstream billing and AR problems.

Qualigenix builds sequestration accounting into every client’s RCM configuration from day one. We ensure CARC 253 adjustments are correctly coded in payment posting, that revenue projections reflect post-sequestration allowed amounts, and that AR aging reports distinguish sequestration adjustments from genuine underpayments requiring follow-up. Our 99% claim accuracy rate and 30% average reduction in AR days mean your post-sequestration revenue is collected as cleanly and quickly as the policy environment allows.

Revenue Cycle Management Services: End-to-end RCM built for Medicare complexity. Visit qualigenix.com/services/revenue-cycle-management-services/

Medical Accounts Receivable Services: AR management that correctly categorizes sequestration adjustments and focuses follow-up energy on recoverable claims. Visit qualigenix.com/services/revenue-cycle-management-services/medical-accounts-receivable-services

Healthcare Performance Reporting: Analytics dashboards that display post-sequestration net revenue, payer mix contribution, and collection cycle performance. Visit qualigenix.com/services/revenue-cycle-management-services/healthcare-performance-reporting/

Denial Management Services: Preventing denials is the single most effective way to ensure you collect every post-sequestration dollar Medicare owes you. Visit qualigenix.com/services/revenue-cycle-management-services/denial-management-services/

Frequently Asked Questions: Medicare Sequestration

What is the current Medicare sequestration rate in 2026?

The current Medicare sequestration rate is 2%, applied to all Medicare Part A and Part B fee-for-service claims under the Budget Control Act of 2011. A potential additional 4% PAYGO sequestration was waived by Congress on November 12, 2025. Providers should budget for the 2% BCA cut as a permanent fixture of Medicare reimbursement through at least February 28, 2033, and model the risk of future PAYGO activation in financial scenario planning.

How is Medicare sequestration applied to claims?

Sequestration is applied post-adjudication. Medicare first processes the claim to determine the allowed amount, then calculates patient cost-sharing (deductibles and coinsurance). The 2% reduction is applied to Medicare’s remaining payment share — not to the total allowed amount and not to the patient’s cost-sharing obligation. The sequestration adjustment appears on the Explanation of Benefits as Claim Adjustment Reason Code (CARC) 253.

Does Medicare sequestration affect patient out-of-pocket costs?

No. Medicare sequestration does not change patient coinsurance, copayments, or deductible obligations. The reduction falls entirely on the provider’s Medicare payment. Patients owe the same cost-sharing amounts as they would without sequestration. The sequestration protection for beneficiaries is explicit in the Budget Control Act and the PAYGO statute — both laws prohibit sequestration from reducing beneficiary benefits or cost-sharing protections.

Does Medicare sequestration apply to Medicare Advantage?

Yes — but differently. For traditional Medicare FFS, sequestration reduces the payment CMS makes directly to providers. For Medicare Advantage, sequestration reduces the capitation payments CMS makes to MA plans. MA plans may or may not pass that reduction through to providers, depending on their contracted rates. Provider contracts with MA plans generally do not reference sequestration directly, so MA plan payment rates are not automatically reduced at the provider level the way FFS payments are.

Has the 4% PAYGO sequestration ever taken effect?

No. The PAYGO sequestration mechanism has been triggered by deficit-increasing legislation multiple times, but Congress has always passed supplemental legislation to waive the cuts before they take effect. The November 2025 stopgap bill waived the PAYGO sequestration that would have been triggered by the One Big Beautiful Bill Act. However, the waiver history should not be interpreted as a guarantee — the political environment and deficit levels make future waivers increasingly difficult to predict.

How does sequestration interact with the 2026 Medicare Physician Fee Schedule conversion factor increases?

The 2026 PFS conversion factor increases (3.77% for QPs, 3.26% for non-QPs) are calculated before sequestration is applied. The published CF figures in the final rule do not incorporate the 2% BCA sequestration reduction. Your actual net payment per service reflects the CF-based allowed amount, reduced by the applicable patient cost-sharing, and then reduced by 2% sequestration. For specialties also affected by the -2.5% efficiency adjustment on Work RVUs, the combined effect may offset most or all of the headline CF increase.

What is the best way to manage sequestration in a medical billing system?

Configure your billing system to map CARC 253 as a contractual adjustment — not an underpayment or open AR balance. Establish a payment posting protocol that identifies and correctly records sequestration deductions on every Medicare remittance. Build post-sequestration net revenue figures into all financial reporting and budgeting. Train your AR follow-up team to distinguish CARC 253 adjustments from genuine underpayments, so that collection resources are focused on recoverable revenue. Qualigenix handles all of this as part of standard RCM setup for new clients.

How can Qualigenix help my practice manage Medicare sequestration?

Qualigenix configures all client billing systems to correctly apply and report Medicare sequestration adjustments from day one. Our healthcare performance reporting dashboards display post-sequestration net revenue alongside gross allowed amounts, giving practice administrators a clear view of their true Medicare income. Our AR management team is trained to distinguish CARC 253 adjustments from recoverable underpayments, ensuring your team’s time and energy is directed at revenue that can actually be collected. Book a free AR assessment at qualigenix.com/contact-us/.

Related Qualigenix Resources

- Revenue Cycle Management Services

- AR Follow-Up Services

- Healthcare Performance Reporting

- Medical Accounts Receivable Services

- Denial Management Services

- Revenue Cycle Management Trends 2026

- What Are RCM KPIs?

- How to Reduce Medical Claim Denials

- RCM KPI Benchmarking

- Accounts Receivable in Healthcare

| Protect Your Medicare Revenue From Sequestration The 2% BCA sequestration is not going away. A future PAYGO cut is a realistic planning scenario. The practices that protect their revenue are the ones with RCM systems built to correctly account for sequestration — not the ones scrambling to diagnose unexplained payment shortfalls 90 days later. Qualigenix offers a free AR assessment to identify where sequestration is (and is not) being correctly managed in your billing workflow. Book at qualigenix.com/contact-us/ |

What’s Next

Real-time eligibility returned active and the claim still denied: the five reasons why

An “active” eligibility result only proves the policy is in force. It never proves the service is covered, that...

Prior authorization turnaround requirements under the CMS interoperability rule: what changed for practices

The CMS interoperability rule (CMS-0057-F) forces impacted payers to decide standard prior authorizations in 7 calendar days and...

Appeal or Write Off? A Decision Framework for Denied Claims Over $500

Don’t let the dollar amount make the call by itself. Sort the denial by reason code, run the...